How's fintech reducing wealth inequality?

26/04/22 by IGOR GORBATSEVICH

Investing

With hindsight, it is truly remarkable how quickly fintech and the concept behind the term has made the leap from the fringe to the mainstream of financial discourse.

Those of us who have been observing and participating in the financial ecosystem over several decades remember the term first appearing in the 1990s, and then only as it applied to some rather abstract and technical ‘back-office’ processes that related to how payments were processed.

Today, London sits at the heart of a global web of disruptive innovation characterised by the increasing interaction of finance and technology. The so-called fintech revolution has already enormous repercussions for everything from how we spend, save, invest, insure, and lend.

The mission that guides us here at Shojin is to ride this wave of dynamic change and to bring as many of the benefits that technology can bring to our specific field of investment expertise – real estate.

What does it mean to ‘democratise’ investing?

One of the most immediate impacts technology can have on the investment world is by opening up more and more lucrative possibilities to the average investor.

Technology-driven innovations like the development of fractional ownership models have meant highly profitable investments that used to be closed to anyone without millions at hand ready to invest are now open to ordinary professionals.

Individual investors can now access online investment platforms and effectively pool their resources to unlock fantastic new investment opportunities. By participating in large-scale, long-term, lucrative investments the dentist, accountant, architect, marketing director, and many other middle-class professionals can claim a seat at the table previously reserved for the global mega-rich.

In this way, the digitisation of finance can and is already leading to a fairer distribution of wealth between the middle-class and the richest 1%, and this revolution has only just started.

What’s so special about real estate?

In a local sense, every middle-class professional has always been aware of the financial advantages of home ownership. Many of the same sound reasons justifying the proportionally vast outlay of capital to purchase a house also operate when the proposal is scaled-up to encompass not just a single house, but an entire apartment block, for example.

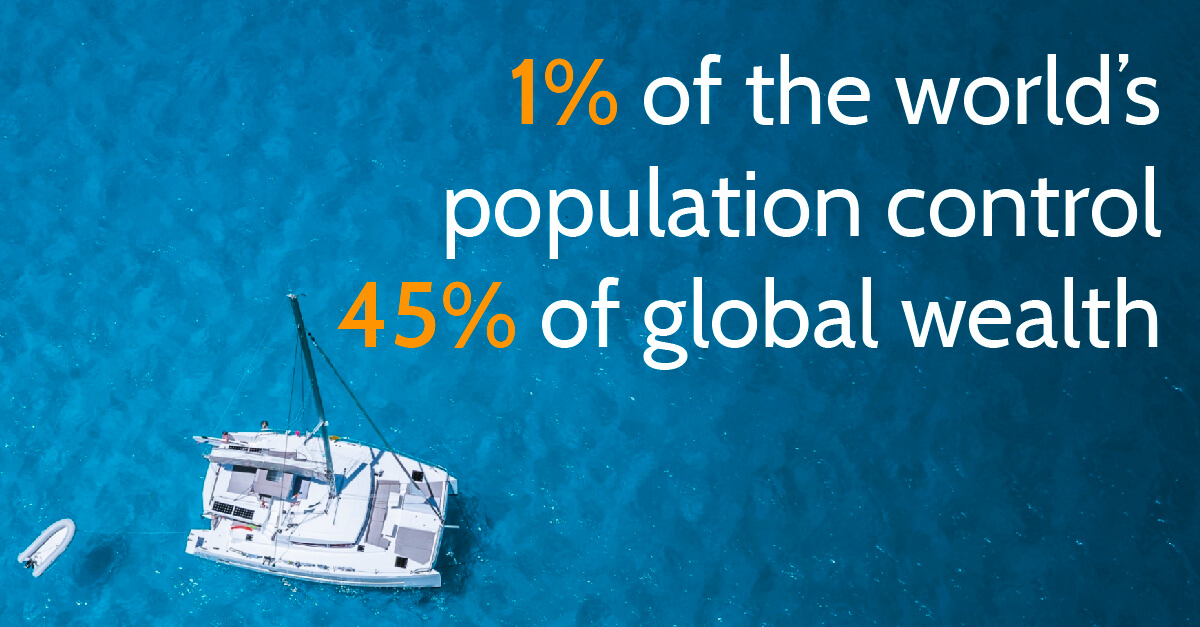

Across the world today, the richest 1% of the adult population control 45% of global wealth. Whilst some of this wealth will have been made through real estate investment, almost all of it is preserved through property.

This is because assets like real estate possess a wonderful combination of attributes that the global mega-rich have always been aware of and known how to exploit to their advantage.

Firstly, property yields income to its owner. Rental income is not only regular and predictable, but can be expected to rise ahead of inflation as well due to its contractual nature.

Secondly, real estate values tend to rise over time. This is, of course, not necessarily a linear or totally predictable process, but over time the value of almost all property will rise once you adjust for exceptional events like the 2008 crisis which sent all house prices spinning downwards for a short time.

Finally, real estate is a boat that rises with the tide, as they say. Ownership of commercial or residential property is a straightforward bet on the economy growing over time and rents continuing to be paid. As we say, exceptional events aside, this is a bet many of us are more than happy to take over the course of our lifetimes.

Why can fintechs like Shojin outcompete more traditional players here?

1. Technology brings down costs for us and for our investors

The first advantage more technology-centred firms have is lower costs. This means we can bring our investment opportunities to a wider audience at significantly lower costs than more traditional real estate investment firms, and we can pass this cost-saving on to our clients.

As with any investment, when costs fall, returns are amplified.

2. Our unique co-investment model

At Shojin we continually refine our combination of advanced fractionalisation techniques which enable small and medium-sized investors to participate alongside larger investors with traditional asset management techniques to ensure the quality of our property projects.

We recognise that new investment propositions for those simply used to holding shares or bonds through an ISA can be daunting, and this is why we invest in every project we offer alongside our clients and with our own capital.

This alignment of interests between us and our investors means we are literally all on the same team, and we will never propose an investment that we aren’t confident enough to put our own capital into.

This is why we can charge zero management fees to our clients, with all profits flowing from a project shared in accordance with the size of each investor's stake.

3. Track-record and expertise

As an experienced property investment company, Shojin has a great deal to offer in terms of our sector-specific investment expertise and knowledge. This means that all our projects undergo a thorough due diligence process, and we perform extensive risk analysis on every project we sign off on. In addition to the prior research, we also directly oversee every project from start to finish, meaning little is left to chance at any stage.

4. Serving an ignored demographic

More than just simply offering a similar service to a traditional firm at a lower cost, Shojin and other fintechs are doing more than this by unlocking new sectors of the investment market.

A market demographic that has traditionally been underserved by the asset management industry are those below the threshold to be considered as high net worth, but who may still have significant amounts of money to invest.

The 9% of the global adult population directly below the richest 1% in the income distribution hold on average between $100,000 and $1 million in investible funds.

These professionals have been left with no or limited access to the large-scale real estate investments those above them have always used to preserve and grow their wealth, and they have rarely been wooed by the asset management industry.

We believe that they, and the rest of the population able and willing to invest for their future, deserve better.